After years of negligible real wage growth, Australian workers are now being told that, because of heightened inflation, they should accept below inflation wage rises — real wage cuts — as anything more would lead to a “wage-price spiral”.

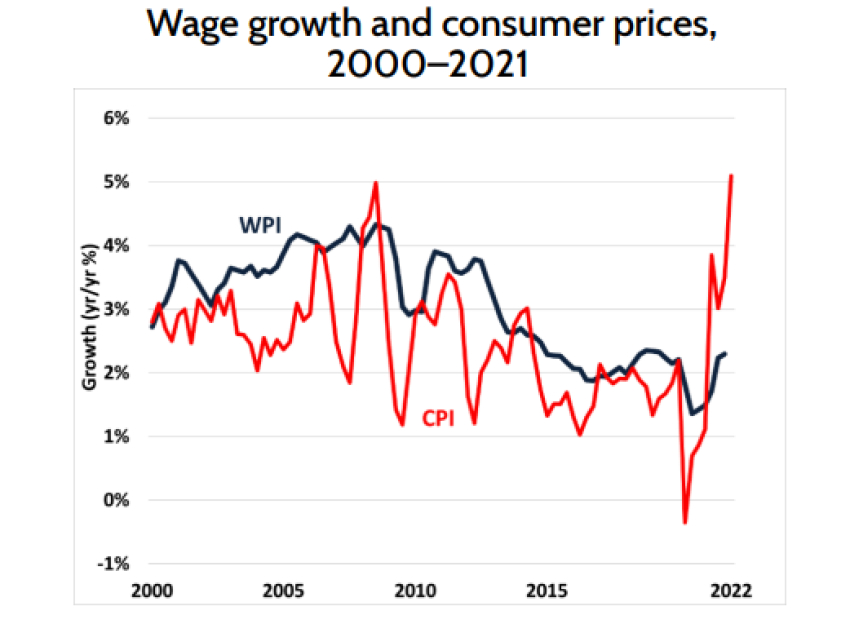

The Australian Bureau of Statistics (ABS) September Quarter Wage Price Index figures put annual wage growth at 3.1%. Its Consumer Price Index figures for the same period put inflation at 7.3%.

That amounts to a 4.2% cut in real wages.

wage_growth_and_prices_australia_institute.png

Coupled with the years of slow wage growth preceding the recent inflationary period, real wages had already dropped back to 2011 levels on the June quarter figures.

However, instead of responding to this by pointing to the need to raise wages to at least keep pace with inflation, politicians, economists, business groups and commentators are urging wage restraint.

They all warn that wage rises will just lead to employers raising their prices to make up for wage rises, in turn leading to further calls for higher wages to catch up with prices — wage and price rises feeding each other in a wage-price spiral.

The idea of a wage-price spiral is commonplace in mainstream economics. The idea even finds backing in more progressive-leaning Keynesian and post-Keynesian economics.

Reserve Bank Governor Philip Lowe warned about the “need to avoid a price-wage spiral” in a November 22 speech, consistent with his previous pronouncements on the issue.

The same sentiment has been echoed around the world, such as by United States Federal Reserve Chair Jerome Powell: “We can’t allow a wage-price spiral to happen, and we can’t allow inflation expectations to become unanchored.”

Prime Minister Anthony Albanese gave support to the idea of wages keeping pace with inflation during the election campaign, begrudgingly backing what appeared to be an off-the-cuff slip during a media conference.

In the event, his government supported a rise in the minimum wage of 5.1% — consistent with the most recent inflation figures at the time although short of where inflation has, predictably, since reached.

The government has not backed calls for wages to keep pace with inflation for the majority of workers who are not affected by the increased minimum wage rate.

In spite of election promises, Treasurer Jim Chalmers said workers should not expect real wages to start keeping pace with inflation until at least 2024.

As for the workers under its direct control, the government is giving the Commonwealth Public Service a mere 3% pay rise.

In other times, employers warn workers that wage rises will mean that they can only hire fewer people and that this will lead to greater unemployment.

Together “wage rises will cause unemployment to rise” and “wage rises will cause inflation to rise” provide justifications for opposing wage increases at almost any time and place.

However, it does not follow that when wages rise employers will, or even can, simply put up their prices at will to offset the rises and maintain their profits.

As in any other time, businesses are restricted in raising prices as they can lose sales.

The extent to which it can be done profitably depends on economic conditions, such as the money supply, productivity and economic growth.

It could be that wage rises will simply mean that employers are forced to accept lower profits.

That is certainly affordable, given that the share of gross domestic product going to workers has been steadily declining for decades to a record low while the share going to profits has moved in the opposite direction.

A new paper, published by the International Monetary Fund (IMF) on November 11, questions the threat of wage-price spirals.

The IMF working paper, titled Wage-Price Spirals: What is the Historical Evidence?, analysed data from advanced economies since the 1960s for significant episodes of rising inflation conjoined with rising nominal wages.

It found 79 episodes to examine and compared them to what might be expected of the normal relationship of wages and prices in the given conditions of employment and productivity levels.

It found that “only a small minority of such episodes were followed by sustained acceleration in wages and prices. Instead, inflation and nominal wage growth tended to stabilize, leaving real wage growth broadly unchanged”.

The report also narrowed in on the episodes more comparable to the current situation, with falling real wages and comparatively low unemployment.

Among these it stated that “sustained wage-price acceleration is even harder to find”.

The report concluded “an important take-away from the analysis is that an acceleration of nominal wages should not necessarily be seen as a sign that a wage-price spiral is taking hold.

“Indeed, history suggests that nominal wages can accelerate while inflation recedes from high levels. In fact, on average, this has happened after similar macroeconomic episodes in the past.”

The enthusiasm in mainstream economics for raising the wage-price spiral threat has always rested on its use as an ideological weapon on behalf of profits against wages, rather than its theoretical or empirical soundness.

This report from a very mainstream source (although it comes with a disclaimer that it does not necessarily represent the views of the IMF) should be a nail in the coffin of the wage-price spiral idea.